tactical asset allocation | insights | June 13, 2024

Sector ETFs: Signal or Noise?¶

Investors and financial news often discuss sector trends and monitor sector performance. For example, on the financial analysis platform koyfin (which is a great Bloomberg terminal replacement btw!), the US Equity Sectors monitor is one of the first things you see. We wondered if this is just noise and best ignored or an important signal you should be watching? How much alpha can you generate and if so, how should you do it? Read on to find out!

Trade Sectors with a TAA Sector Rotation Strategy¶

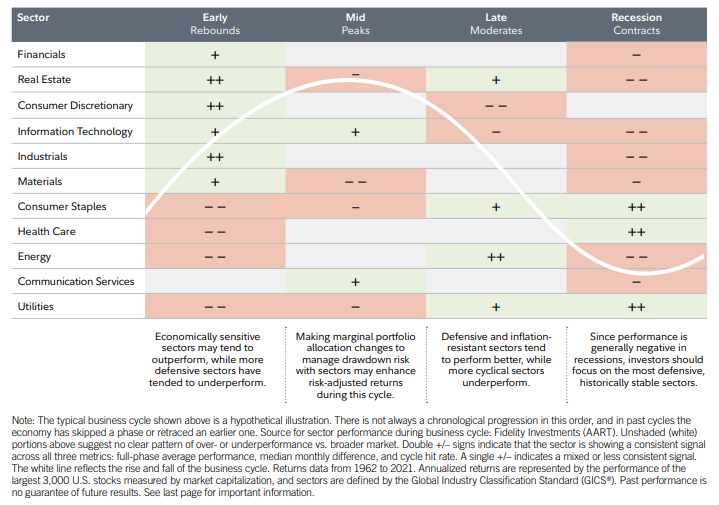

For those unfamiliar with the topic, tactical asset allocation (TAA) strategies aim to take advantage of sector trends. A tactical asset allocation strategy is an investment approach that actively adjusts the allocation of assets in a portfolio to take advantage of market opportunities or to protect against potential market downturns. Unlike strategic asset allocation, which maintains a long-term, fixed asset mix based on an investor's risk tolerance, goals, and time horizon, TAA involves short- to medium-term adjustments to asset weights based on market conditions, economic trends, and other factors.

One tactical approach to managing a portfolio is an ETF sector rotation investment strategy that involves shifting investments between different sectors of the economy at various times to capitalize on changing economic cycles and market conditions. The goal is to improve portfolio performance by investing in sectors expected to outperform and reducing exposure to those expected to underperform. For more details see Fidelity An introduction to sector rotation strategies.

Just for comparison here is the buy-and-hold sector performance.

Portfolio Holding Details by sector¶

The charts below show the holdings for each sector over time. Interestingly sectors that are usually considered "low beta, non-cyclical" were not necessarily traded when typical sector rotation frameworks tell you to do so. We will write more about that in the follow-up.

Existing Sector Rotation ETFs are underperforming¶

As mentioned the crystal ball strategy can't actually be traded because you don't know the sector performance ahead of time. We found two sector rotation ETFs that you can actually buy and checked their performance. Both are active ETFs that were only recently issued. Unfortunately both of them were unable to capture the alpha potential and underperformed the market over that short period.

Lets see if we can do better with ML!